This article is about a company that looks attractive at face value. Once you go deeper, you will see big potential pitfalls. I will talk about the need to study the business before you start working with the numbers. You will also see some interesting accounting tricks that you should be aware of.

Why did I look at SRF Ltd.?

I looked at this company a few months back. It had a high dividend yield (dividend divided by market capitalization). If one gets a dividend yield of 6-7% in a stock and if the dividend will not be cut in the future it is almost like putting your money in a fixed deposit of around 10% (for someone in the 30% tax bracket). Dividends are tax free.

This does not take into account the possible capital appreciation if the company’s outlook is good.

If you see something like this, it is worth investigating.

What does SRF Ltd. do?

Technical Textiles

- Tyre Cord

- Belting Fabrics

- Coated Fabrics

- Industrial Yarn

- Laminated Fabrics

Chemicals

- Fluorochemicals

- Fluorospecialities

Packaging Films

Engineering Plastics

SRF Ltd.’s corporate presentation is a good starting point to understand the business.

SRF manufactures industrial products. Usually in industrial products it is not easy to generate high return on capital unless you have some compelling competitive advantages which are sustainable. As Warren Buffett calls them, you need moats.

I recalled that SRF had been a “hot” stock in 2004-06. The stock had a huge run-up because of the carbon credits story.

What are carbon credits?

Under the Kyoto Protocol, many nations came together and decided to deal with the problem of carbon emissions. These emissions contribute to the greenhouse effect and global warming. Nations agreed to cut down on emissions in two ways.

One is where some nations asked their industries to cut down emissions by upgrading to better technology or closing down polluting plants. The other is where polluters could “pay” for emission reductions done by someone else.

The intermediate currency for this “payment” is carbon credits.

Polluting industries from developing nations have cut down emissions in a large way (also in a distorted way, more about that in this article). In return for cuts, they receive carbon credits.

These carbon credits are sold on exchanges. Usually buyers from developed nations buy these carbon credits. In a way, without actually reducing emissions at their end, they are “paying” for reduction done by someone else.

One important point to note is that carbon credits does not imply only carbon dioxide (CO2) emission reduction. It is applicable to multiple different processes and gases which can cause global warming. In fact, there are many gases which are more harmful than CO2 in terms of their potential to trap heat in the atmosphere.

Why did SRF Ltd. get carbon credits?

SRF manufactures fluorochemicals. Think of refrigerants as an example. If you remember there was a lot of controversy over chloro-fluoro carbon (CFC) gases long back. These were used in refrigerator and AC compressors.

SRF manufactures a fluorochemical called HFC -22. HFC-23 is a by-product of HFC-22 production. This is a greenhouse gas, which is 11,700 times more potent than a similar quantity of CO2 in the atmosphere.

SRF used to release the by-product HFC-23 into the atmosphere without any treatment. Around 2004, SRF started incinerating HFC-23. This was an example of reduction of greenhouse gases. They applied under the Kyoto Protocol and got carbon credits for their project.

United Nations Clean Development Mechanism link for SRF HFC-23 project

How did SRF account for these carbon credits?

This is where the story gets more interesting.

I opened the annual report (AR) for FY12. This was a few months back and the AR for FY13 had not been released at that point.

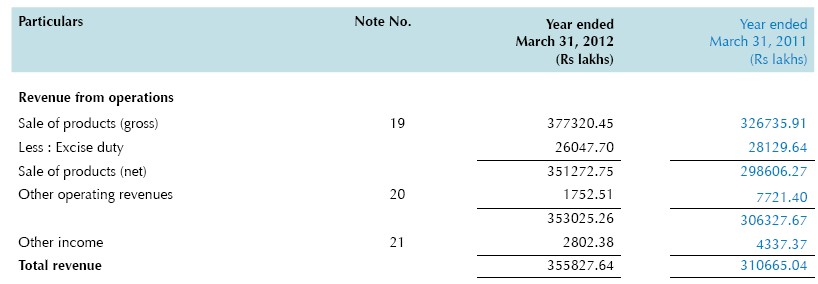

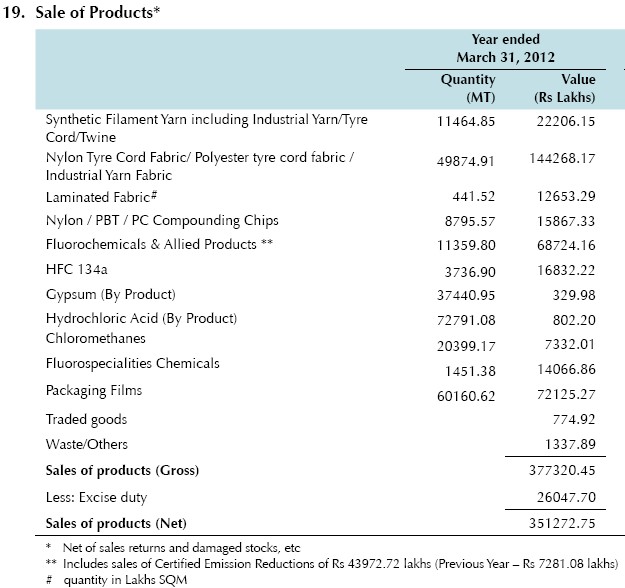

If you go into Note No. 19, you will see the sales breakup.

Notice anything atypical?

Carbon credits are a source of income for SRF. Why are they not listed as a separate income head? Common sense says that they should be in other income (it is not a core activity, it is incidental). That is a separate discussion since accounting standards are still not clear on this topic.

Anyway, we need to ask is carbon credit income substantial?

Yes.

Read the note at the bottom of the table. Certified Emission Reductions (CER) is the technical name for carbon credits. The amount generated from sale of CERs is Rs. 43972 lakh. This is around 12% of the company’s sales in FY12.

Why is CER hidden away in notes when there are much smaller sales items than CER?

What is the impact of CERs on profits of SRF Ltd.?

CER’s would not have a large manufacturing expense associated with them like other manufactured products. My understanding is that the bulk of the money generated from the CER head in the breakup will be directly contributing to the Profit before Tax (PBT).

If I take this assumption, it contributes to a relatively large 77% of PBT.

If you read the annual report, the biggest takeaway is that underneath the hood, there is a completely different engine. The bulk of profits are coming from CERs and not the core manufacturing business.

What has been the performance of SRF in the past if we go by the books of accounts?

| FY09 | FY10 | FY11 | FY12 | |

|---|---|---|---|---|

| Return on Equity | 14% | 26% | 29% | 21% |

At face value, it looks like a decent set of figures. One may call it capital efficient.

What is the performance of SRF if we adjust and remove the impact of CER sales?

Figures are in Rs. lakh

| FY10 | FY11 | FY12 | |

|---|---|---|---|

| Total Sales(as per accounts) | 224,923 | 310,665 | 355,827 |

| Total Sales(adjusted for CER) | 198,967 | 303,384 | 311,854 |

| Total Expenses | 179,532 | 242,917 | 299,241 |

| EBITDA | 39,452 | 83,406 | 39,190 |

| PBT | 19,435 | 60,467 | 12,613 |

| Tax (assumption – 30%) | 5,831 | 18,140 | 3,784 |

| PAT | 13,605 | 42,327 | 8,829 |

| EBITDA (%) | 20% | 27% | 13% |

| PAT (%) | 7% | 14% | 3% |

| Return on equity | 11% | 26% | 5% |

I subtracted the CER sales (remember the figure I saw in the notes, I had to pull more of them from old annual reports, they are not presented directly) from the Total sales.

I kept the expenses same (recall the assumption I made about the CER expenses)

I re-calculated tax. This is important because if I consider that there is no CER income, tax outgo should reduce with lesser taxable income.

Notice the return on equity figure now captures the manufacturing business only. CERs are not in the picture. RoE is fluctuating and not steady at all.

Worse, RoE of 5% means the shareholders’ funds are earning less than they would if kept in a bank.

This clearly proves that this company looks attractive on the face of it. If it has to continue having good RoEs and good dividend payouts we have to check the CER sales.

Are they sustainable?

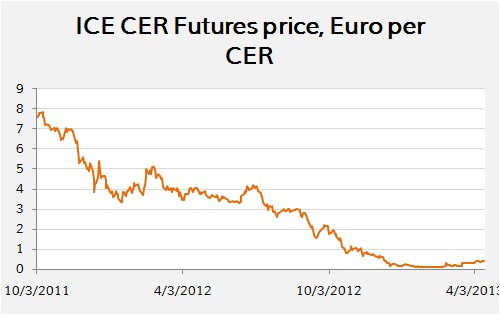

CER price

It was worth checking how the market for CERs is behaving.

Source: Intercontinental Exchange

CER prices have fallen badly over the last few years. As of October 2013, they are trading around EUR 0.34 per CER on the futures market. Possible reasons that I read included, the oversupply of CERs from developing countries including India and China combined with general slowdown in the Eurozone (less pollution) which leads to less demand in terms of the CDM mechanism. The Eurozone is a big market for CERs under the CDM process.

So, clearly price is not in SRF’s favour.

SRF’s CER volume

If you revisit the UN CDM link I have given above, you will see that the period for the project under the UN CDM is July 2004 to June 2014.

Back of the envelope calculation will tell you that SRF can earn around Rs. 20 crore till June 2014 for the balance CERs, at today’s rates of CER. In comparison in FY12, they clocked Rs. 439 crore in sales.

Between Sep 2012 and Jan 2013, SRF generated 1.38 mn CERs. They have “claimed” only 0.1 mn. This may be because of low prices in the CER market. This is the only time in the last 29 periods from the 2004 that they have claimed less.

Can SRF renew their project and sell CERs again in the future?

To put it crudely, will the hen that laid the golden eggs continue to be kind?

I dug up some more data on HFC-23 and the CDM process.

In Sep 2012, the UNFCC released this statement,

Source: Report of the High-Level Panel on the CDM Policy Dialogue, under the UNFCC

European Commission speaks out

- Allowing credits from the destruction of HFC-23 can create a perverse incentive to continue to produce or even increase production of it and of HCFC-22, a gas which both depletes the ozone layer and is also a powerful greenhouse gas.

- The environmental integrity of the credits is therefore questionable.

- These projects do not provide value for money as they could have been funded and implemented more cost-effectively by other means. Because of the credits they receive, the rates of return are exorbitant – revenues from the sale of HFC-23 credits to EU ETS participants can represent up to 78 times the initial capital investment and operational costs of the project.

- The EU considers that emission reductions which can be achieved relatively cheaply – as with destruction of HFC-23 from HCFC-22 production and N2O from adipic acid production – should not be financed through the international carbon market. They should be undertaken by developing countries themselves as part of efforts to reduce their own emissions. Alternatively, the actual per-tonne cost of reductions could be directly funded.

Source: http://europa.eu/rapid/press-release_IP-11-56_en.htm

In plain speak,

- People are producing HFC-22 not because there is a good market for HFC-22.

- They are selling it for the by-product HFC-23.

- Perverse incentives are at play.

Read this article from DNA – Are toxic gases being created just to earn carbon credits?

Let me be clear that I am not pointing fingers at SRF specifically. It is HFC-22 which has come under pressure.

Whatever be the case, it does not look like there are going to be golden eggs after June 2014.

What does a CER-less future mean for SRF?

| FY09 | FY10 | FY11 | FY12 | |

|---|---|---|---|---|

| Operating cash flow | 45,406 | 60,699 | 76,299 | 83,062 |

| Adjusted operating cash flow adjusted for tax | 24,386 | 18,169 | 5,097 | 30,781 |

| Capex | 38,546 | 35,639 | 20,201 | 49,537 |

| Free cash flow | (14,160) | (17,470) | (15,104) | (18,756) |

I adjusted the operating cash flow downwards for the past few years. The results are not surprising. Without CER sales, they could not have enough cash to grow the core business, without taking on debt or raising equity. And that too, for a business which has low return on equity.

Without CER sales in the future, how can they grow? How can they generate sufficient free cash to pay dividends to shareholders?

This is the reason why my article had this title. I get the feeling that I am walking towards the edge of a cliff.

Conclusion

- First, try to understand the business in depth.

- Go beyond the usual profit and loss statement, balance sheet and cash flow statement. Sometimes they are like veils.

- The notes give the true picture in many cases.

If you have come across any other case relating to accounting, please share it using the comments below. It would be useful to the Capital Orbit Community.

Further reading

Read the CDM Policy Dialogue – Sep 2012

Read the report by Carbon Trust – Global Carbon mechanisms

Hi Kunal,

Please publish such long detailed posts about economy, businesses, individual stock stories. I wanted to invest in SRF a few months back and was advised not to because of carbon credits issue. I did not dig so deep and do such a thorough analysis as you have done. Thanks a lot.

Hi Bhaskar,

Suggestion taken. I enjoy long articles too.

Good to know that you stayed away. This stock has tanked in recent times. 🙂

You are welcome.

Regards,

Kunal

Good analysis Kunal!

-Prakash

Thanks Prakash. Glad to know you liked it. Have you come across any more cases like this? If yes, do share.

Regards,

Kunal

Hi Kunal,

Avoided getting into SRF a few months back even though it looked good on the surface since it was carbon credit play mainly. The base business isn’t that lucrative due to volatility in input costs & other reasons. As you rightly mentioned, this was a hot stock back then – it featured in Forbes Apr 2011 issue.

Since you mentioned dividend yield, you might want to have a look at ILFS investment managers. It had a terrific dividend yield a year back too but as you say one needs to dig deeper to see the potential pitfalls.

Hi Himanshu,

True. The base business is average.

I had looked at IL&FS Investment Managers. I am not sure whether I want to put money into it. Parag Parikh’s new mutual fund has a position in IL&FS. Actually all of their investments are what traditional “value” investors would do.

I tend to go more with the definition of value investing espoused by Buffet and not necessarily the Benjamin Graham kind. I think what Buffett invests in encompasses Graham too. Plus much more.

What other stocks do you find interesting?

I have my own reservations regarding PPFAS Fund. One, their PMS hasn’t performed great (~15% since inception) & given that PMS is a “premier” sort of product. Many mutual funds have averaged better than that over a 5-7 year period. Second, their investments are “traditional” value investing types (more graham type) . At some point in their investing career, many value stalwarts have shifted from a deep value to economic moat/fisher/munger investing style (more sustainable). Prof Bakshi has some really good articles on this & has written over how his approach has also changed over the years.

Making money Buffett style – either one has to have a good base (sizable investment corpus) or is willing to defer consumption till his later years (& assuming to outlive many :)). Compounding is no doubt the eight wonder but the base effect also comes into play. Even if one was reasonably certain of prospects of stocks like Cera, PI Inds, Gandhimathi Appliances 10 years back, would they have put 10 – 20% of their capital into them then?

Among their current holdings IGL, Novartis & Wyeth look interesting to me. Kunal if and when time permits could you please do some analysis of non mainstream pharma companies like Novartis, Wyeth, FDC, Aarti Drugs.

Bhaskar, I have not looked at all the pharma companies you have mentioned. I was pretty interested in FDC. I hear the promoters are conservative and good to shareholders. But the last time I looked, the business was not growing at a decent clip.

I will stay away from Indraprastha Gas. It is nothing to do with the recent Supreme Court case. I think there is too much chance of govt. interference and politics. I will probably expand on this in an article.

In a nutshell, do you want the company’s prices to be at the mercy of politicians. Gas is an essential item in consumption for many urban people. What stops a Kejriwal from launching a dharna tomorrow? It is just a outlier event in terms of probability but I don’t like it. I might be wrong.

I will be more comfortable with companies that are exposed to the market and can price their goods with less interference from anybody.

Ok. I did not check their PMS returns. Is the 15% return before or after fees? You are right. There are mutual funds which have delivered returns in that range too at lower expense ratios, I presume.

I would still respect them for their conviction. That they don’t change investing styles based on what is “hot” right now.

The broader question of which style is better will never be answered. There will be investors with different views on each of these styles. Let us live and let live 🙂

The “good base” part is something that I hear a lot about. Don’t you think one should aim at percentage returns and not absolute returns. With time, the “base amount” will increase.

I heard this from a reader. He says he has Rs. 5,000/- to invest in the market. I said don’t bother with how small or large the amount is. Look for percentage returns. In time, you will increase your corpus as you earn more from your salary (or business income). Now, percentage returns will yield absolute amounts which will look much better than the amounts you have when you invest Rs. 5,000/-

Most importantly, start off right.

About the Cera, PI Industries question. I might not put 10% in one company of that size 10 years back. But I can pick up a bunch of companies like this and allocate a part of my portfolio to them. That will be better. Some will not do so well. Some will grow well. Allocate more to them along the way.

Excellent analysis. Thanks Kunal.

Thanks Sagar!

Hi Kunal

Good analysis. I did looked at SRF, but decided not to look at it because of the nature of business and no competitive advantage…I am posting below Lumax Tech eg., just to highlight another example of how detailed analysis of number can help. Let me tell at the outset that very very few people have agreed to my analysis of Lumax and its quite possible that my whole conclusion is WRONG…Purpose is not to recommend sell or buy but just an example. [I did post this analysis on another blog, long back]

**********************

In my opinion headline numbers in case of Lumax Auto Technologies are totally misleading and I do not see any competitive advantage which enables company to earn better profits than its group company Lumax Industries.

1) A large part of EBITA [> 50%] is contributed by trading activity and other miscellaneous income like labour charges [which was included in sales].

2) Company has entered into numerous related party transactions [sales > 20% to related parties] which raises question on the reliability of reported numbers.

3) Lumax Industries [another group company and a listed entity] which is exactly in same business as Lumax Auto technologies had EBITA margin between 2-4% during last five years and simple average of last five years is 3% whereas Lumax Auto technologies EBITA margin for last two years is around 7.5%-8%.[[look at standalone number for Lumax Auto, subsidiary is engaged in providing brake and parking assembly]

4) Further [this point is not that serious but still raised many questions] while Lumax Auto technologies has classified part of sale to Lumax Industries under finished goods, Lumax Industries in its accounts do not show any purchase of finished goods. Under Lumax Industries accounts, entire thing is shown as purchase of raw materials. The deeper you analyse the numbers, the suspicion deepens. I have attached break up of trading goods, which just does not make sense. In some years, some items shows losses and in some years abnormal profits.

Please download PDF from here https://docs.google.com/file/d/0B8Mr8IuAEwz7eHdZdzRzWUxBRUU/edit?usp=sharing&pli=1

Hi Anil,

First, thanks for sharing a very detailed analysis. It’s interesting. I had approached this stock with interest because it seemed cheap. But the related party transactions and the relatively commoditized business did not interest me too much. You have, of course, gone far deeper than I did. It should be useful to other readers.

Things like the same item being reported under one name in one company and it being treated differently in the other company is striking.

Thanks!

Very nice analysis, Kunal. The CER story is well known, though, and is reflected in the stock price.

However, I do feel that you are being a bit too harsh on the stock.

Basically, what these companies were doing were that they were making an excess of HCFC-22, and then incinerating the HFC-23, which was produced as a byproduct.Obviously, this led to an overproduction of HCFC-22. But it was not entirely costless, as you assume, though the margins were pretty high. Also, this was to a certain extent compensated by keeping the price of HCFC-22 low, because excess HCFC-22 was produced to create more HFC-23. Lots of Indian and Chinese companies have done this.

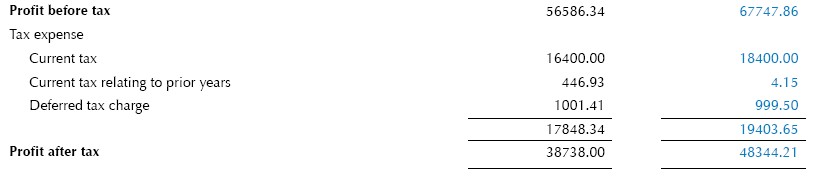

You have used figures from the AR 2011-12. AR 2012-13 is also out. Within sales of over 3000 crores CER sales account for 262 Crores. CER sales declined to 262 Crores from 439 crores, a difference of 177 Crores. Profits before tax actually fell from 565 Cr. to 352 Crores, a larger decline. SO CER is not the only profit lever. The industrial economy is too.

However, as the Q1 results indicate (which don’t have any CER income), their profits this year should further fall from 352 Crores to 175 Crores. In the meantime, they have used this extra money generated to put up several new plants, while not adding significantly to debt. These plants should begin to contribute from this fiscal onwards. The share price has corrected commensurately. (Disc: I bought a reasonable quantity at Rs. 128-135). Even after the recent run-up in the price, the share is still only around 5 times estimated earnings for 2013-14. These earnings are in a terrible industrial economy. Surely these will improve when the economy turns around, and the new plants get commissioned.

So clearly, while the earlier price (which at one time was around 400+) was clearly not justified in the absence of CERs, I think the current price is fair for a company with good management, long pedigree, and a reasonable balance sheet ( Debt is around 800 crores, cash and equivalents around 200 Crores). Lots of Chemical companies of this sort are trading at 6-10 times earnings. Atul is a company with almost the same size and profitability as SRF, and it has a PE multiple of 8.

Based on my reading, the dividend this year should halve. This will still give a decent dividend yield of 4% on the CMP. And if the economy improves, the PE should expand along with expanding profits. Otherwise, you are stuck with a company with an EV/EBITDA value of 3.5 or therabouts, which is not a bad place to be.

Hi Samir, thanks for taking time out for a very detailed comment. You have put in quite some work here. I fully agree with you that they have carried out a lot of capex with the CER cash. I don’t find the core business very interesting.

Anyway, we can have different views. Else there would be no market 🙂

You might want to check on the sale of part of their business in 2001 and subsequent buying back of the same business from a group company. I was not too enthused when I analyzed it in detail. I didn’t like it.

This will be a good starting point. http://ajayshahblog.blogspot.in/2009/05/need-better-information-for-minority.html

I urge you to do your own research on this point since you have put money behind this stock. Check the group companies and ARs from 2007-09. There is a lot of info. there.

Nevertheless, it’s great to see anyone who bothers to do a deep study of a stock. I hope that we interact more ahead. It was a pleasure to read through your analysis.

Thanks, Kunal for the info.

Your blog entry (and my subsequent study) did help me to clarify a few things. I have decided to sell about 25% of my holdings prior to Q2 results.

Regards

Samir

Hi, Kunal

Seems like I was pretty accurate with my expectation of results.

Yes, results dipped. I didn’t check the stock performance though.

Hey Kunal

Sold off my entire SRF stock yesterday. Still don’t think it is a bad buy, and it certainly wasn’t at my purchase price of around 130, but just thought that there were better opportunities out there.

Currently investing in Munjal Auto, Selan Exploration and IDFC.

Hi Samir,

Good to know! I agree that there are better opportunities.

If you have a 3-4 time frame IDFC is not bad at all at present levels. I have a done a quick study. I have yet not done a detailed reading.

I recently invested in Atul Auto and Accelya Kale.

Regards,

Kunal

Great analysis! Can you recommend some good value stocks? Especially pharma, because I don’t hold a single stock in that sector. Not that I have to. Any tips would be great! Many thanks in advance.

Hi Uma,

You can check the articles on Cera Sanitaryware, Supreme Industries and Swaraj Engines. I don’t get into specific recommendations. I share views. Again, I only recommend that you invest in a stock if you can understand the business. So, tips, might not be the best way forward. I hope you take it in the right spirit. I mean well.

Regards,

Kunal

SRF went like a rocket from 165 to 320 after your post, up almost 100% in just 6 months.

Yes, another reader pointed out the same! 🙂

My view does not change though unless there is demonstration of business strength sans carbon credit based income.

Kunal,

thanks a lot for this article. It helps to understand investments for people like me, who are starting with investments. Recently, even I faced a similar situation. I found opto circuit financial statement very interesting. I found that operating profit was around 40% etc. So bought a few shares. but one thing that caught my attention was tax. though they were claiming 244.88Cr PBT, they were paying only 3Cr tax (according to Warren buffett, this indicates some problem ). after digging deep, I figured out that they have a cash receivable problem. I know what I discovered was a very simple thing. but for a starter it was a great discovery!.

I wanted to check one thing. I have not received any mail from you after Feb10. Is it because my email id is de-listed from your website? I am missing the educational mails you send. please let me know if I need to do re-register in your website to receive mails again.

thanks and regards

Sharvari

Dear Kunal,

I came across your blog while searching for something and swa this article on SRF Ltd.

Read it. But found the research to be too shallow or in a hurry to achieve a pre-conceived result. Why I say this is because you completely missed out on the speciality fluorochemicals business of this company. They utilized CER income to nurture and grow a high value added business.

Anyway, the bus is already on the run. I am not saying above aftee the event, I have been saying this for last two years through various reports and presentations.

Would be happy to connect with you and see how we can learn from each other as value investors.

Regards,

Rahul Agarwal

Discovered your website today itself.

Going through your atticles from last 2 hours.

I must say your analysis and understanding of business is comparable to mr bakshi.

Great work.

Abhishek